Foreign employees working in China have access to a wide range of financial services in China, but they also have certain obligations. One such obligation is paying tax on their personal income. The following article breaks down this important topic.

Just like in their home countries, foreigners working in China are required to contribute some portion of their salary and add to their employers’ liability. The two most common channels for employee contributions are:

- Social benefits

- Individual Income Tax

Learn more about payroll services in China

Social benefits

The Social Security system in China consists of four different insurances that are applicable to foreign employees:

- Pension fund

- Medical insurance

- Industrial injury insurance

- Unemployment insurance

Since 2011, foreign employees also participate in the payments’ contribution, of course in lower amounts compared to their employers. Also, the contribution rates slightly vary between locations (e.g., while in Beijing, Shenzhen, Nanjing, etc. foreign employees are obligated to pay social benefits, Shanghai does not formally require foreign employees to pay).

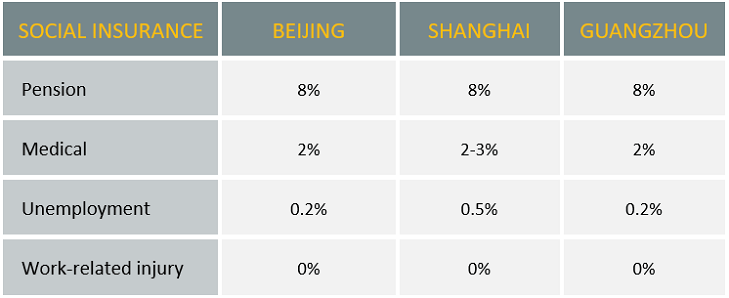

The following is a breakdown of the social insurances’ contribution rates paid by foreign employees in three different cities:

Note: Remember that despite similar percentages in some categories, the employers’ contributions in these categories vary.

For more information on HR services in China, and employee services in China, read our HR regulations guide for foreign companies in China.

Social insurance exemption is granted to eligible employees coming from one of the 12 countries with which China has a special agreement: Canada, Denmark, France, Germany, Finland, France, Japan, Luxembourg, Netherlands, South Korea, Spain and Switzerland.

Individual Income Tax

Foreigners living and working in China are required to pay taxes on their income. The tax payment has to be filed on a monthly basis, by the 15th following the end of each month. The total amount of tax payable is determined by two factors:

- Time of residence in China (affects the sources of incomes on which tax is imposed)

- Tax rate (varies between different level of incomes, progressive tax)

Naturally, the longer the taxpayer resides in China, the higher the salary, and so the tax payable increases.

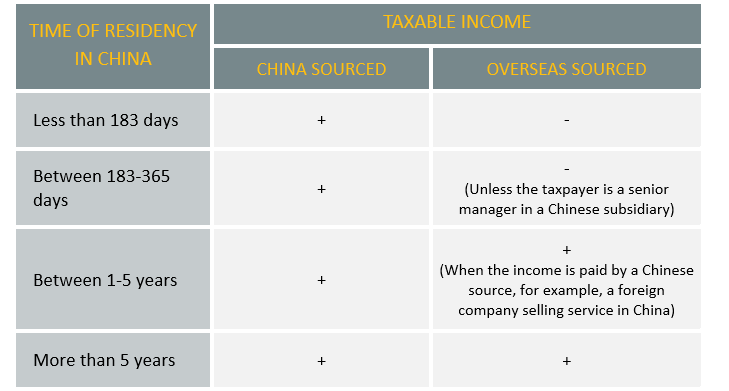

The following is a breakdown of the taxable income derived from the length of time spent in China by the foreign taxpayer:

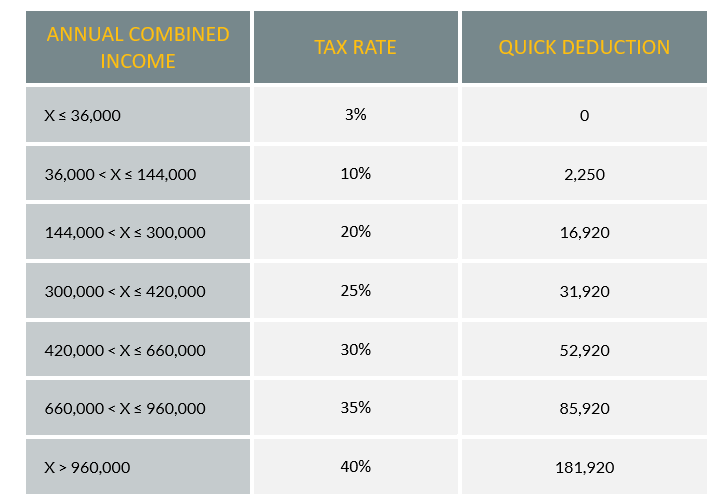

Tax rate

The tax rate changes between different income levels. The following table shows the different degrees of tax percentage (the annual combined income and the quick deduction are in RMB)

Formulas

The last stage is the final calculation, taking into consideration the aforementioned data.

- Monthly taxable income:

Monthly income – 5,000 RMB (standard deduction) – allowances

- Tax payable:

Monthly taxable income X tax rate – quick deduction

Tax Benefits

As the first table demonstrates, 183 days is the lowest threshold that turns a foreign employee into a “tax resident”. Once they qualify as such, they are entitled to pay IIT on both China and overseas-sourced incomes. However, they are eligible for significant tax-exempt benefits in eight different categories (housing rental expense, education expenses for children, language training expense, meal fee, laundry fee, relocation expense, business travel expense, and home leave expense). As these benefits are tax-free, expats can enjoy them without impacting their basic salaries (on which taxes were levied). This policy is set to remain in effect until December 31st , 2027.

At PTL Group, we specialize in financial services in China. Get in touch today and let us support your China operations.

Last updated: Feb 2026